This educational article is intended to spark thoughtful reflection and friendly public conversation. I hope you find this information as eye-opening as I did while researching it. Too often, we find ourselves arguing passionately about topics we don’t fully understand. Taking a few minutes to read this piece will give you the foundational knowledge needed to make a much stronger, more educated point on the subject.

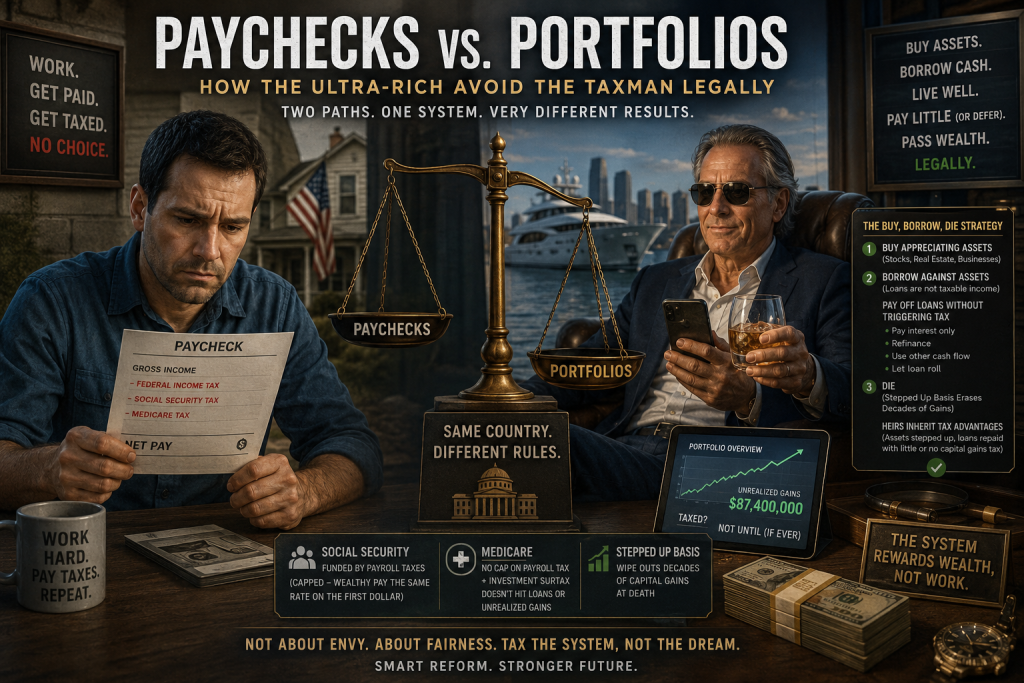

For most working Americans, taxes are immediate and visible. A person works, gets paid, and federal income tax, Social Security tax, and Medicare tax are usually taken out before the money ever reaches the bank account.

For the ultra wealthy, the system can work very differently. Their financial lives are often built around assets, not paychecks. Instead of relying mainly on wages, they may own stock, real estate, private companies, trusts, and other investments that grow in value over time.

That difference matters because the U.S. tax system does not simply tax people based on whether they are described as poor, middle class, wealthy, or rich. It taxes different types of money in different ways. Wages, investments, loans, inherited assets, and business income all follow different rules.

Disclaimer: The author of this article is a researcher, not a CPA or licensed financial professional. This article is a summarized compilation of in-depth research shared for informational purposes only, and should not be taken as financial advice.

The article explains some of tax rules in plain language for educational and informational purposes. By sticking to the facts and avoiding personal bias, it allows readers to draw their own conclusions. The focus is on legal tax structures: why they exist, how they impact public programs, and why reforming them is highly complex.

How the Ultra Wealthy Avoid or Delay Taxation

When people hear that billionaires can pay little or no income tax compared with the growth of their wealth, the explanation usually begins with one simple point: the tax system does not tax most asset growth until the asset is sold.

If someone earns a salary, that income is taxed in the year it is earned. If someone owns stock that rises in value, that increase is usually not taxed right away. The gain exists on paper, but it is considered unrealized until the stock is sold.

That is where the basic strategy often called “Buy, Borrow, Die” begins.

“Buy, Borrow, Die”

Step One: Buy or Build Assets

The ultra wealthy often hold large amounts of wealth in assets that can rise in value. These may include company stock, real estate, private business interests, investment funds, or other holdings.

If those assets grow from $10 million to $100 million, the owner is much wealthier. However, unless the owner sells the asset or receives taxable income from it, the growth itself usually does not trigger income tax.

That is different from a paycheck. A worker cannot choose to delay taxation on wages already earned. A paycheck is income when paid. Asset growth, by contrast, can remain untaxed for years if the owner keeps holding the asset.

Step Two: Borrow Against the Assets

The next step is access to cash.

If the asset owner sells stock to raise money, that sale may create a taxable capital gain. Long term capital gains are usually taxed at lower rates than ordinary wages, but a large sale can still create a significant tax bill.

Instead, wealthy asset owners may borrow money using their investments as collateral. These loans may come through securities backed lines of credit, private banking arrangements, or similar lending structures.

Borrowed money is generally not taxable income because it must be repaid. A loan is debt, not earnings. This is the same basic reason a homeowner does not pay income tax when taking out a mortgage or a home equity loan.

For wealthy borrowers, the difference is scale and access. A person with hundreds of millions in stock may be able to borrow millions at favorable terms without selling the stock. That creates spending money without creating a taxable sale.

The natural question is how those loans are paid off without creating the same tax problem later. The answer depends on the loan terms and the borrower’s financial structure. Some large asset backed loans do not work like a regular car loan or personal loan with fixed monthly principal payments. The borrower may pay only interest, refinance the loan, borrow from another line of credit, use dividends or other lower taxed investment income, or allow interest to be added to the loan balance if the lender permits it.

As long as the collateral remains strong enough, the bank may be willing to keep the loan open because the borrower’s assets provide security. This allows the borrower to keep accessing cash without selling the underlying asset and without triggering capital gains tax at that time.

The strategy is not risk free. If the asset value falls too much, the lender may demand more collateral or force a sale. If interest rates rise, the cost of borrowing increases. But when the borrower has extremely large and diversified assets, the loan can sometimes be managed for years, refinanced, or carried until death.

Step Three: Hold Until Death

The last part of the strategy involves inheritance rules.

Normally, if someone buys stock for $10 and later sells it for $100, the $90 gain may be taxable. But when assets are inherited, the tax basis is often adjusted to the fair market value on the date of death. This is commonly called stepped up basis.

If the owner bought stock for $10 and died when it was worth $100, the heir’s new tax basis may become $100. If the heir sells it shortly after inheritance for $100, there may be little or no capital gain for income tax purposes.

This can also help resolve the outstanding loans. After death, the estate or heirs may sell part of the inherited assets to repay the lender. Because the basis may have stepped up to the current market value, that sale may create little or no capital gain for income tax purposes.

This is why the full strategy is described as “Buy, Borrow, Die.” The person buys or builds valuable assets, borrows against them instead of selling, and then the estate may use inherited asset rules to settle debts with reduced or no capital gains tax on the appreciation that occurred during life.

This can erase decades of built in gains from the income tax system. Estate tax may still apply to very large estates, but the federal estate tax exemption is high, and advanced planning can reduce exposure for some families.

Paychecks and Portfolios Follow Different Rulebooks

The tax code does not officially divide people into the paycheck class and the asset class. But in real life, the distinction helps explain why many people feel the system treats workers and asset owners differently.

| Tax Area | Paycheck Income | Portfolio Based Wealth |

|---|---|---|

| Main source of money | Wages, salary, hourly work | Stock, real estate, business equity, investment assets |

| Tax timing | Usually taxed immediately through withholding | Often taxed only when sold |

| Social Security tax | Applies to wages up to the annual wage cap | Does not apply to capital gains or loans |

| Medicare tax | Applies to wages, with no wage cap for basic Medicare tax | Investment income may face separate surtax only when realized |

| Access to cash | Spend after tax wages or borrow against income | Borrow against assets without selling them |

| Inheritance treatment | Retirement accounts may remain taxable to heirs | Many appreciated assets may receive stepped up basis |

This does not mean all wealthy people pay no tax. Many high income households pay large federal income tax bills. It also does not mean all asset owners avoid taxation forever. Selling assets, receiving dividends, operating businesses, or transferring very large estates can create tax obligations.

The concern is narrower. The rules can allow some ultra wealthy households to live on borrowed money, delay taxable sales, and pass appreciated assets to heirs with much of the built in gain removed from income tax.

Why Capital Gains Are Taxed Differently

There are several policy reasons Congress has historically taxed long term capital gains differently from wages.

One argument is investment. Lower capital gains rates may encourage people to take risks, fund businesses, invest in real estate, and support economic growth.

Another argument is inflation. If an asset is held for many years, part of the increase in value may reflect inflation rather than true profit. A lower rate is sometimes defended as a rough way to soften that effect.

A third argument is double taxation. Corporate profits may already be taxed at the corporate level. When those profits increase the value of stock or are paid to shareholders, taxing them again at the full wage rate is viewed by some as excessive.

Critics respond that these arguments may justify some preference for investment, but not a system where large gains can be deferred for life and then erased at death.

Impact on Social Security

Social Security is funded mainly through payroll taxes. Workers and employers each pay a Social Security tax on wages up to the annual taxable maximum.

That structure creates a major difference between wages and investment wealth. A worker pays Social Security tax on earned wages up to the cap. A billionaire living mainly on asset backed loans or unrealized stock growth pays no Social Security tax on that growth because it is not wage income.

This matters because Social Security faces long term financing pressure. If Congress does nothing, the combined Social Security trust funds are projected to be unable to pay full scheduled benefits in the 2030s.

That does not mean Social Security disappears. It means incoming revenue would still support most benefits, but not all scheduled benefits, unless Congress changes taxes, benefits, borrowing rules, or some combination of those options.

Some reform proposals would raise or remove the wage cap. Others would restart payroll taxation above a higher income level, creating what is sometimes called a donut hole. The goal would be to collect more from very high earners while avoiding new taxes on middle income wages.

Impact on Medicare and Health Programs

Medicare is funded differently from Social Security. The basic Medicare payroll tax applies to all wages, with no wage cap. Higher income taxpayers may also owe additional Medicare related taxes, including the net investment income tax on certain realized investment income.

The challenge is that unrealized gains and borrowed money usually do not count as taxable investment income. If a wealthy person borrows against stock rather than selling it, the borrowing may avoid both capital gains tax and investment surtax at that time.

That limits the ability of investment surtaxes to reach some forms of wealth growth. At the same time, Medicare’s Hospital Insurance Trust Fund also faces long term pressure as health costs rise and the population ages.

Reformers argue that more consistent taxation of very large asset based income could strengthen Medicare funding. Critics warn that poorly designed rules could reduce investment, complicate estate planning, and create valuation problems for private businesses and family owned assets.

Impact on the Broader Economy

The current system has both benefits and costs.

Supporters of lower investment taxes argue that keeping more capital in private markets helps fund businesses, startups, innovation, job creation, and retirement investment growth. They also warn that aggressive taxes on unrealized gains could force asset sales, reduce market liquidity, and affect retirement accounts tied to stock markets.

Critics argue that the current system concentrates wealth at the top and leaves too much pressure on wages. They also argue that dollars held in large portfolios may circulate less through local economies than dollars earned and spent by working families.

Both arguments have merit. Capital is important for business growth. Consumer spending is also important for local communities. A stable tax system has to raise enough revenue without punishing work, discouraging productive investment, or allowing the wealthiest households to permanently avoid tax on gains that support their lifestyle.

Middle Ground Reform Options

1. Restart Social Security Payroll Tax Above a High Income Level

Instead of raising taxes on every worker, Congress could keep the current wage cap and restart Social Security tax only above a much higher threshold, such as very high earned income.

This would leave most workers untouched while asking the highest wage earners to contribute more to the system.

2. Treat Very Large Asset Backed Loans as Taxable Events

Some proposals would treat very large loans secured by appreciated assets as a taxable event when the borrowing is used for personal liquidity.

The idea is not to tax ordinary mortgages, home equity loans, or small personal loans. The idea is to address large scale borrowing that substitutes for selling assets and realizing gains.

3. Limit Stepped Up Basis for Very Large Estates

Another approach would preserve stepped up basis for ordinary families, modest homes, and small estates, but limit it above a high exemption level.

For assets above that level, heirs could receive the original tax basis instead of a full reset. Taxes would not necessarily be due immediately at death, but the built in gain would eventually be taxed when the heir sells.

4. Create a Higher Capital Gains Tier for Very Large Gains

Congress could keep current capital gains rates for most investors while adding a higher rate only for people realizing very large annual investment gains.

This approach would protect ordinary retirement investors while narrowing the gap between wage taxation and elite investment income.

Public Perception vs. Hard Math

Public frustration with the tax system is real. Many Americans believe wealthy people and large corporations do not pay enough. Many also feel their own taxes are too high for the services they receive.

That creates a difficult policy paradox. The public often wants lower taxes for working families, higher taxes on the ultra wealthy, stronger Social Security, stronger Medicare, better infrastructure, and less national debt.

The math does not allow every goal to be met by slogans alone. A modern government cannot fund everything only by taxing a small number of billionaires. At the same time, a healthy economy cannot rely too heavily on workers while allowing the largest asset gains to avoid tax indefinitely.

The fairest path likely sits between those extremes. It would protect regular workers, avoid punishing ordinary investors, preserve incentives for productive business growth, and close the specific legal pathways that allow the largest fortunes to grow, be borrowed against, and pass through generations with limited income tax exposure.

Final Takeaway

The central issue is not simply rich versus poor. It is labor versus capital.

Paychecks are taxed immediately. Portfolio wealth can often grow quietly, be borrowed against, and be transferred under rules that reduce or erase capital gains tax.

That structure is legal. It is also one reason tax fairness remains one of the most debated economic issues in America.

Understanding the mechanics helps move the discussion away from anger and toward better questions: What should be taxed? When should it be taxed? How much should be protected for ordinary families? And how can the country fund essential programs without damaging the economy that supports them?

Sourcing Section

- IRS Federal Income Tax Rates and Brackets

Official IRS explanation of progressive tax brackets and how higher rates apply only to the next layer of taxable income, not the full income amount.

https://www.irs.gov/filing/federal-income-tax-rates-and-brackets - IRS 2026 Tax Inflation Adjustments

Official IRS release confirming 2026 standard deductions, marginal rate thresholds, and the $15,000,000 estate tax basic exclusion amount for 2026.

https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill - SEC Accredited Investors

Official SEC explanation of accredited investor financial criteria.

https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/accredited-investors - IRS Topic No. 409, Capital Gains and Losses

Official IRS explanation that net capital gains may be taxed at lower rates than ordinary income.

https://www.irs.gov/taxtopics/tc409 - IRS Net Investment Income Tax Questions and Answers

IRS explanation of the 3.8 percent Net Investment Income Tax and income thresholds.

https://www.irs.gov/newsroom/questions-and-answers-on-the-net-investment-income-tax - IRS Topic No. 432, Cancellation of Debt

Official IRS explanation that loan proceeds are not included in gross income when there is an obligation to repay the lender.

https://www.irs.gov/taxtopics/tc432 - IRS Publication 551, Basis of Assets

IRS publication explaining basis rules for inherited property.

https://www.irs.gov/publications/p551 - CBO: Change the Taxation of Assets Transferred at Death

Congressional Budget Office explanation of stepped up basis, carryover basis, and possible taxation of unrealized gains at death.

https://www.cbo.gov/budget-options/60943 - SSA Contribution and Benefit Base

Social Security Administration source confirming the 2026 taxable maximum and OASDI tax rate.

https://www.ssa.gov/oact/cola/cbb.html - SSA Trustees Report Summary

Official trustees summary showing Social Security and Medicare trust fund projections.

https://www.ssa.gov/oact/trsum/ - CBO Distribution of Household Income, 2022

CBO analysis of household income, transfers, federal taxes, capital income concentration, and federal tax progressivity.

https://www.cbo.gov/publication/62300 - Pew Research Center Tax Frustrations Survey, 2026

Pew survey showing public frustration with perceived tax fairness, tax complexity, and personal tax burden.

https://www.pewresearch.org/short-reads/2026/04/06/top-tax-frustrations-for-americans-feeling-that-some-wealthy-people-corporations-dont-pay-fair-share/ - Yale Budget Lab: Buy Borrow Die Reform Options

Policy analysis discussing reform options for borrowing against appreciated assets.

https://budgetlab.yale.edu/research/buy-borrow-die-options-reforming-tax-treatment-borrowing-against-appreciated-assets